Cell Sampling in Monetary Unit Sampling offers a nuanced approach to auditing, blending precision with efficiency. This blog post delves into how Cell Sampling enhances the traditional MUS process, providing auditors with a more granular level of analysis. We’ll explore the methodology behind Cell Sampling, its advantages, and practical applications within the broader scope of MUS. Join us as we uncover the strategic benefits of incorporating Cell Sampling into your audit toolkit.

The Basics of Cell Sampling

Cell sampling is selecting a sample of monetary units from a population. In cell sampling, the population of monetary units is divided into subsets or cells, and an independent selection is made in each cell. It is similar to systematic sampling, but in cell sampling, a separate sample of a monetary unit is made within each interval (cell), thus avoiding potential bias associated with systematic sampling.

The method is simple, ensures the desired sample size, avoids bias associated with systematic sampling, and distributes the sample evenly across the entire population.

In the following section, we’ll elaborate on how to perform cell sampling in the audit.

Implementing Cell Sampling in Monetary Unit Sampling

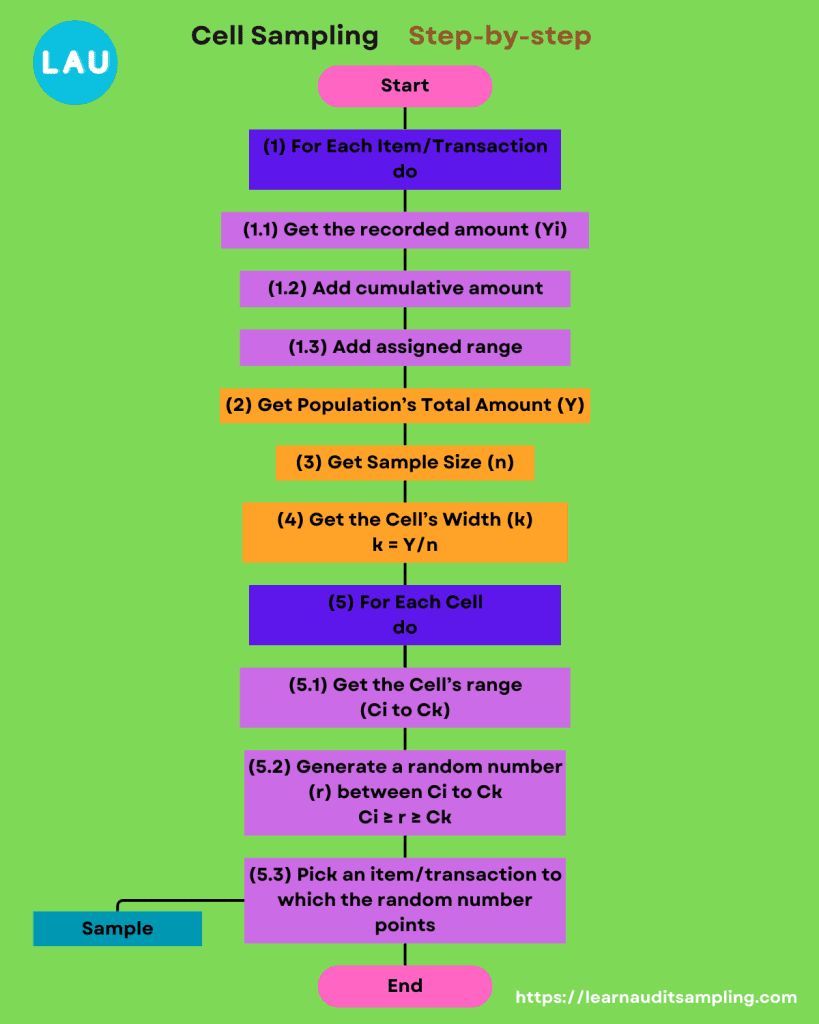

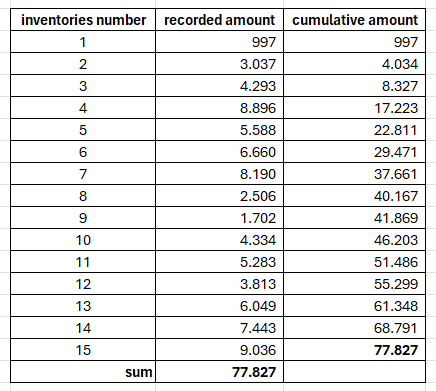

This is the step-by-step process of performing cell sampling. For example, you have 15 items in the inventory population. For each inventory, you should have the recorded amount (step #1.1). Then, you add the cumulative amount (step #1.2). You may use the below image as a reference.

After adding the cumulative amount column for every inventory item, add the assigned range (step #1.3). The assigned range column will help identify which item (or logical unit when using the following image’s term) is pointed by the random number.

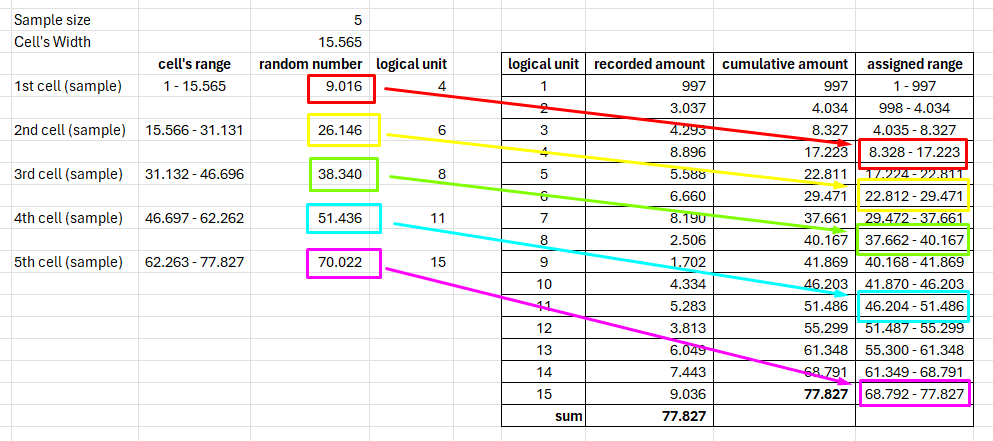

The population recorded amount (step #2) and sample size (step #3) help compute the cell’s width (or sampling interval). You’ll get the cell’s width by dividing the population recorded amount by the sample size.

The cell size will be the same as the sample size in the cell sampling method; this differs from the Sieve sampling, where the actual sample size could be greater or lesser than the planned sample size.

For each cell, four cells in the previous image, you must assign its range (step #5.1). The lower range is the first number in the cell; thus, the upper range is the first number added by the cell’s width.

Generate a random number between the lower and upper range (step #5.2). And for the last step, select items to which the random number points. For example, the first cell has 9.016 as a random number generated; ergo, you’ll pick item #4, which has an assigned range between 8.328 and 17.223, including 9.016.

Repeat the process until you get all the samples.

Advantages of Cell Sampling in Monetary Unit Sampling

After reviewing the process, you’ll better understand the nuance of the sampling selection method. Below are the advantages of Cell Sampling, mainly when applied in Monetary Unit Sampling.

- It’s simple.

- It results in precisely the sample size desired.

- Enhanced Representativeness: By dividing the population into cells and selecting a sample from each, cell sampling ensures a more uniform and representative coverage of the entire population. This method helps in capturing a broad view of the population’s characteristics.

- Reduced Sampling Bias: The systematic approach of cell sampling minimizes the risk of bias in the selection process. Since samples are drawn from evenly distributed cells across the population, it reduces the likelihood of over-concentrating on specific segments.

- Improved Detection of Misstatements: Cell sampling can improve the detection of misstatements across different population segments. Ensuring that all segments are sampled allows you to identify errors or irregularities that might be missed in a more concentrated sampling approach.

- Flexibility in Application: This method offers flexibility to auditors in terms of defining cell sizes and adjusting the sampling approach based on the characteristics of the audit population. This adaptability makes it suitable for a wide range of auditing situations.

- Efficiency in Audit Planning: Cell sampling can streamline the audit planning process. Auditors can plan their audit procedures more efficiently and effectively, knowing that each population segment will be represented in the sample.

- Facilitates Risk Assessment: By providing a comprehensive overview of the entire population, cell sampling aids auditors in assessing the risk of material misstatement. This thorough insight supports more accurate risk evaluations and audit decisions.

- Ease of Understanding and Explaining: The straightforward nature of cell sampling makes it easier for you to explain the methodology and rationale behind your sampling decisions to stakeholders, enhancing transparency and trust in the audit process.

Challenges

As you may think, Cell Sampling also has challenges to be considered. Here are some.

- Complexity in Implementation: Setting up a cell sampling approach can be more complex than traditional sampling methods. Determining the optimal cell size and ensuring each cell is defined correctly requires careful planning and understanding of the population.

- Increased Administrative Effort: Managing the sampling process across multiple cells, especially in large or diverse populations, can increase the administrative workload. Tracking and documenting the selection from each cell adds layers of complexity to the audit process.

- Potential for Overlooking Small Misstatements: While cell sampling effectively ensures representativeness, it might not always capture more minor misstatements if they are spread thinly across the population. This could lead to underestimating the cumulative effect of such misstatements.

- Difficulty in Handling Non-Uniform Populations: In populations where value concentrations are highly non-uniform, determining the appropriate cell size and ensuring each cell is equally represented can be challenging. This may lead to inefficiencies in sampling and possibly skew the sample’s representativeness.

- Resource Intensiveness: Depending on the size and complexity of the population, cell sampling may require more resources in terms of time and manpower compared to more straightforward sampling methods. This could impact the overall efficiency of the audit process.

Comparing Cell Sampling to Other Monetary Unit Sampling Methods

There are several sampling selection methods in the Monetary Unit Sampling realm. For example, simple random sampling, systematic sampling, sieve sampling, and Lahiri sampling. Here are some aspects that separate cell sampling from other methods.

- Independent selection within intervals: In cell sampling, a separate selection of a monetary unit is made within each interval, whereas in systematic sampling, the units occur at the same relative position in each interval. This reduces bias potential and avoids regularities and patterns in error patterns.

- Precision: Cell sampling is more precise than simple random sampling in all cases. It also results in exactly the desired sample size and avoids any risk of bias associated with systematic sampling.

- Distribution across the population: The sample in cell sampling is distributed evenly across the entire population, which can lead to more representative samples.

- Selection probabilities: The selection probabilities of cell sampling are derived differently from other sampling methods, leading to potential differences in the precision and accuracy of the estimates.

Conclusions

Cell Sampling in Monetary Unit Sampling is relatively easy to use and offers representativeness. Those two alone can enhance your confidence in your audit conclusion. Other benefits, such as a more precise sample size, help you manage audit resources better. Combining all the benefits, considerations, and auditee’s condition gives you a new challenge for each audit, which by the end of the day, will improve your audit quality.

Integrating Cell Sampling into MUS showcases the evolving landscape of audit practices. It underscores the importance of adopting innovative approaches for more accurate and reliable financial audits. As auditors, staying abreast of these advancements is crucial for your continued success and growth.

Elevate your auditing skills by staying informed. Subscribe to our newsletter for the latest insights and updates on audit techniques. Join our community of forward-thinking professionals committed to excellence in auditing. Subscribe now and never miss an update.