Systematic Sampling in Monetary Unit Sampling enhances audit accuracy and efficiency. This blog post explores the integration of systematic sampling with MUS, highlighting its methodology, benefits, and how it can streamline the audit process. We’ll cover the essential aspects of this approach, providing you, the auditors, with the knowledge to implement this technique effectively and achieve more reliable audit results. Discover the advantages of systematic sampling within the MUS framework and how it can elevate your auditing strategies.

Understanding Systematic Sampling in Monetary Unit Sampling

Systematic sampling isn’t a method exclusively used in the audit realm. It’s a general statistical method. Wikipedia, define systematic sampling as a statistical method in survey methodology that involves the selection of elements from an ordered sampling frame.

This technique ensures that each element in the population has a known and equal probability of selection, making systematic sampling functionally similar to simple random sampling (SRS). However, it’s important to note that systematic sampling is not identical to SRS because not every possible sample of a specific size has an equal chance of being chosen. Despite this, systematic sampling is often more efficient than SRS, significantly if the variance within a systematic sample exceeds the variance of the population.

When digging in the audit sources, systematic sampling often defined as a probabilistic method of sampling in which the auditor calculates an interval based on the size of the population and the desired sample size. The auditor then selects the items for the sample based on the size of the interval and a randomly selected number between zero and the sample size.

This method is advantageous because it allows for quick drawing of samples and puts the numbers in sequence. However, a significant problem with systematic sampling is the potential for bias, as once the first item in the sample is selected, all other items are chosen automatically, which could lead to a non-representative sample if the characteristic of interest is not randomly distributed in the population. We’ll talk later about the advantages and challenges of the said method.

In my opinion, it’s the most prevalent sampling method in Monetary Unit Sampling. The AICPA Audit Audit Sampling Guide and several well-known audit books, such as Arens and Whittington, endorse it.

The Role of Systematic Sampling in MUS

Systematic sampling is a sample selection method, meaning we use the method to pick a sample from the population of an item or transaction. When employing Monetary Unit Sampling in the audit engagement, after selecting the sample size, you then choose the sample; that’s when systematic sampling (or another sample selection method) comes into the scene.

In statistics, choosing the correct sample selection method is as important as other aspects, e.g., calculating the sample size or extrapolating the sample’s result to the population. Using the least appropriate sample selection method may lead to a biased or less representative sample. Ergo, getting the inaccurate audit conclusion.

Advantages of Systematic Sampling in MUS

Below are several advantages of systematic sampling.

- Systematic sampling covers a population and can have the same effect as random sampling if the errors are spread randomly.

- This method can be employed with a random starting point and selecting every nth item, simplifying the sampling process. The approach automatically puts the numbers in sequence, making it easy to implement.

- Systematic sampling can be more practical in situations where it is difficult to access a completely random sample or where there are constraints on time and resources.

- It can benefit large populations, providing a systematic approach to selecting a representative sample.

- When errors are spread randomly throughout the population, systematic sampling can result in a representative sample.

Implementing Systematic Sampling in MUS

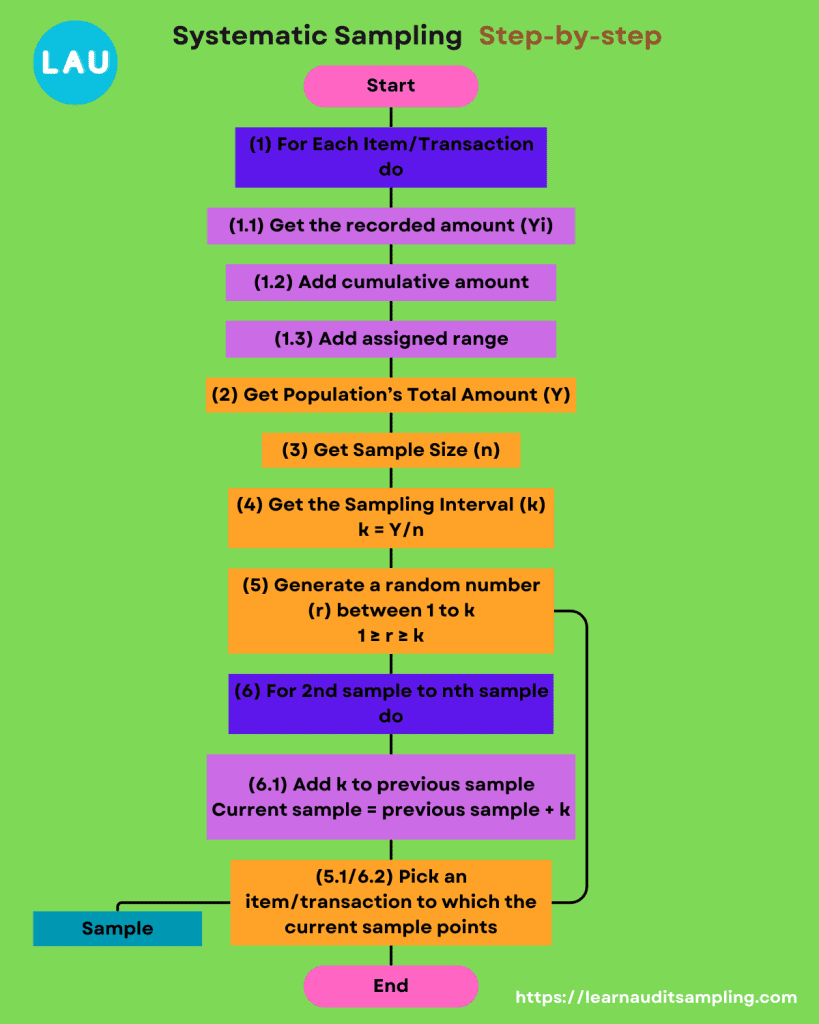

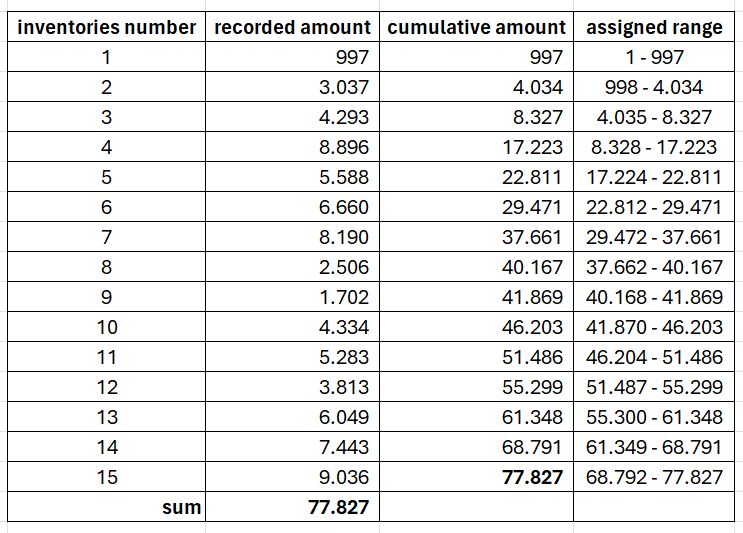

The previous image shows the algorithm or step-by-step systematic sampling. Let’s use the inventory population of 15 items for better clarity, as shown below. You’ll pretend to audit the inventory. For each item (or transaction), you need to get the recorded amount (step #1.1), add the cumulative amount column (step #1.2), and then add the assigned range column (step #1.3).

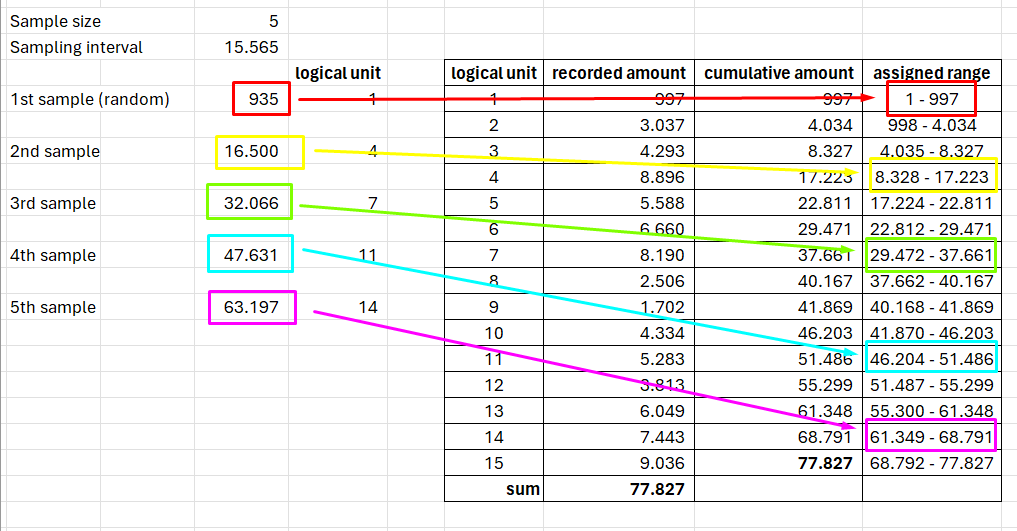

The population’s total amount (step #2) and the sample size (step #3) were then used to calculate the sampling interval (step #4). This time, you get 15,565 as the sampling interval.

How do you draw the first sample? It’s by generates a random number between 1 and a sampling interval (step #5). In the example, you get 935 as the random number. Using the number, you look at the assigned range column to identify which logical unit/item/transaction to pick (step #5.1).

Selecting the rest of the sample is relative easy. Keeps adding the first generated random number (935) with the sampling interval (15,565) and you’ll get the next sample (step #6.1). Don’t forget to convert the number in the assigned range into logical unit/item/transaction number (step #6.2),

Challenges

After gaining familiarity with the method’s mechanics, naturally, you’ll spot the benefits and challenges of the technique. It would help to consider several challenges before applying systematic sampling in your audit engagement.

- If the errors (item/transaction with error) are not spread randomly throughout the population, systematic sampling may not result in a representative sample, as Gray and Arens pointed out. If the errors are clustered in a particular section of the population, systematic sampling may not capture this effectively. Another point to consider, as AICPA, Arens, and Horgan pointed out, is since the method involves selecting every nth item from a list, it may inadvertently skip over specific patterns or anomalies in the data, leading to a non-representative sample.

- The sample might be biased; thus, you should use multiple random starting points if the population is not in random order. Whittington says it. This may add another complexity and demand more resources for the course.

- The method may not be suitable for populations with a high degree of variability, as it may not effectively capture the full range of variation within the population.

- In the more extreme scenario, Hoggduin et al. suggest you avoid using systematic selection in MUS applications. They said, “When applying MUS with systematic selection, we see material errors more frequently than we’d like. Interestingly, the reliability of our risk assessments takes a hit when the sampling interval width narrows, errors tainting magnitudes, and errors are increasingly concentrated around higher-value population members.”

Conclusion

Systematic Sampling is a popular sample selection method, especially when Monetary Unit Sampling is employed in the audit engagement. The method is endorsed by authoritative audit organizations and authors. No wonder it is already embedded in several audit tools.

I believe there is a high chance you have already used systematic sampling in your audit. That creates a need for understanding the method for yourself, your colleagues, and the auditees. In this blog post, we already covered the method’s advantages, step-by-step when using it, and the challenges that need to be aware of.

On the other flip, the method mechanics expose us to a biased sample. In the end, let me reiterate our magic spell: it depends on the auditor’s (your) professional judgment, whether to use systematic sampling or another sample selection method.

Stay ahead in the auditing world by subscribing to our newsletter. Get the latest updates on advanced auditing techniques and insights in your inbox. Join our community of forward-thinking auditors committed to excellence. Subscribe now and transform your audit approach with cutting-edge strategies.